We Are A Leading UK Commercial Energy, And Sustainability Consultancy

Middle East Market Update: 9th March 2026

Latest Updates for Middle East Conflict for the 9th March 2026.

Let Us Contact You:

Market Update:

- Friday saw market prices close higher than Thursday.

- This morning, once again we’re seeing a further increase, with oil breaking $100/bbl.

- UK gas & power prices have risen significantly with the front two seasons now c.16% higher than Friday’s close, while power is also c.15% higher.

- The Middle East status quo remains. Ongoing attacks continue, whilst the Straits of Hormuz remains effectively closed, continuing to impact supplies and world markets.

NATURAL GAS:

Gas prices have opened strongly this morning, with the Middle East situation escalating over the weekend, pointing towards a longer term conflict with more risk for a wider regional conflict bringing more disruption to global energy markets.

The Apr-26 contracts across Europe gapped up impressively, with TTF Apr-26 increasing €8/MWh to push back above €60/MWh. The NBP contract climbed 21p/therm from 135p/therm to 156p/therm. The gains have not been limited to the front of the curve this morning, with Cal-27 THE contract also finding support, lifting by around €5/MWh to reach €43/MWh.

Iran have chosen a new Supreme Leader, with Mojtaba Khamenei replacing his father who was killed in the opening wave of attacks. Analysis suggesting that this is unlikely to bring any material change in the regime that the US and Israel had hoped, pointing towards a more drawn out conflict.

Other states in the Gulf have been the target of strikes across the weekend, with Saudi Arabia and Bahrain energy infrastructure impacted. Bahrain have announced a force majeure following the attacks.

With no end in sight with the conflict, the bottle neck and supply disruption through the Strait of Hormuz is starting to impact further dated commodity contracts as global energy comes under pressure to meet demand.

In other news, European temperatures are set to remain mild with North Western Europe set to hold above seasonal average for the working week. Renewable generation will drop this week bringing some increase to gas demand for power generation.

ELECTRICITY:

Power prices have followed gas and global commodities upwards this morning taking direction from the ongoing Middle East conflict.

Wind generation is set to hold below seasonal average for the first half of the week across the UK, Germany, Netherlands and France likely to bring CCGT and other fuels into the fuel generation mix. With increasing gas costs, power contracts have also climbed.

Solar generation is expected to be poor for the next two days with German solar set to fall by around 600MWh, which could tighten supply a touch.

French nuclear capacity remains low for March in comparison to February, with total capacity available at 48GW today, down by 4GW from last month.

Carbon EUAs Dec-26 also posted gains, bringing further support to electricity prices further along the curve in what is a bullish start to the week for the wider energy complex.

Brent Crude has opened extremely strongly this morning with the tensions in the Middle East seemingly escalating. Strikes across energy infrastructure has expanded with Bahrain calling force majeure and wider oil production slowing down. Brent pushed up from around $90/bbl to $120/bbl and is on track for a biggest intraday move in history.

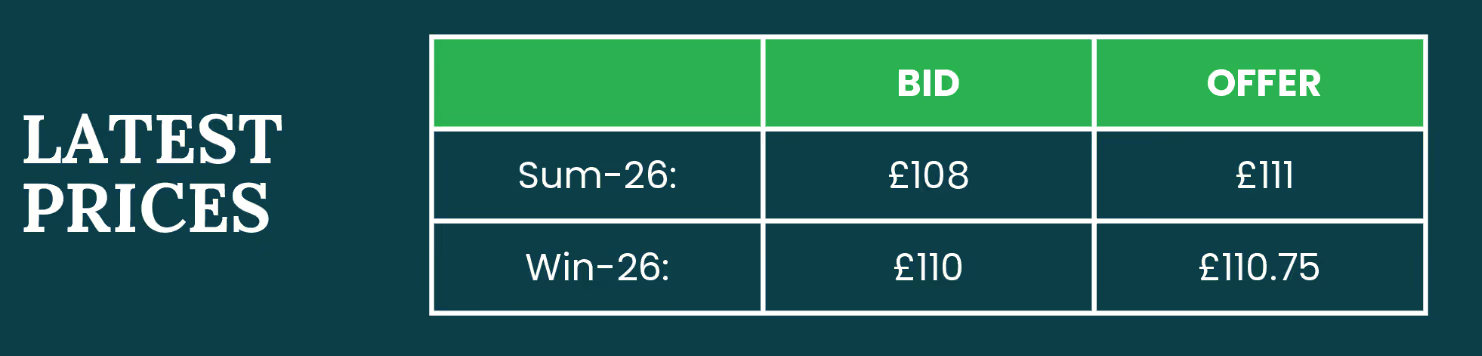

Latest Price:

Latest Gas & Power Annual Chart:

Speak With Us

We understand the complexities of navigating your energy, book in a time to speak with us below

Book A Consultation

Get In Touch